If we’re serious about painting the North American future we keep talking about — the one where Mexico supercharges U.S. growth, nearshoring turns into a continental manufacturing renaissance and we stop worrying about distant supply chains — then we have to start where everything else begins: energy. Without it, there are no factories, no AI servers, no data centers, no EVs, no production, no jobs, no growth. Nada.

When we look at what’s happening in the Middle East and its implications for Asia, Europe and basically the entire planet, we’re facing a classic “tsunami moment.” The ocean pulls way back, the beach looks weirdly inviting and most people just stand there taking selfies instead of running for higher ground. That’s exactly where we are with global energy. Tomas Pueyo laid it out in chilling detail: by 2050, the Middle East will be a geopolitical mess — civil wars in Iran, Kurdish breakaways, Iraqi splintering, Azerbaijan in flames — because the oil that funded everything is drying up.

Europe and Asia, still hooked on those distant barrels, are about to get slammed (really, read Mr. Pueyo here). And if Mexico sits on its hands, Venezuela and Guyana (with their own massive reserves) will happily step in and become the region’s new energy and petro-suppliers.

Wake-up call, folks. The ocean is already receding. But here’s the beautiful part: North America doesn’t have to play that game.

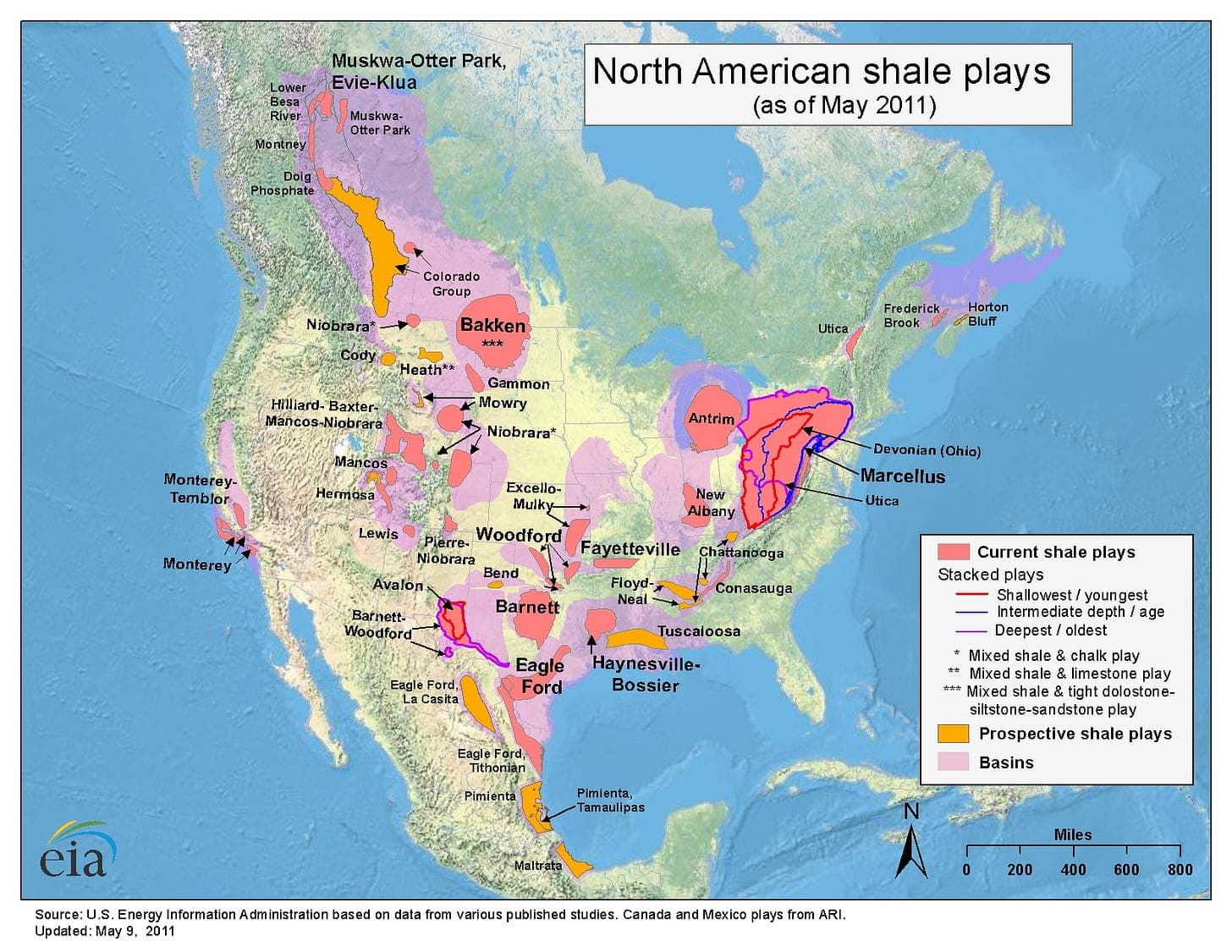

We have something no other bloc can match: genuine regional complementarity that feels almost unfair. The United States sits on world-leading natural gas production and enough reserves to power domestic needs and exports for decades. Canada holds the planet’s third-largest proven oil reserves.

And Mexico? NREL’s numbers still blow my mind: more than 28,000 GW of technical renewable capacity across solar, wind, geothermal, and hydro. That’s enough to meet Mexico’s electricity needs a hundred times over.

Put those three together and you get a perfectly balanced continental battery: U.S. gas for baseload reliability, Canadian oil for the heavy stuff, Mexican sunshine and wind for the cheap, scalable, zero-fuel-cost future. Energy security? Check.

Industrial competitiveness? Check. A real energy transition that doesn’t bankrupt anyone? Double check.

We’re already living the first draft of this story, and it’s working better than most people admit. Mexico imports 73% of its natural gas — 99% of that via pipeline straight from Texas. Those pipelines have grown 8.3% a year since Trump’s first term.

Flip the script, and Mexico is America’s top export market for petroleum products, natural gas, refined fuels, and the fourth-biggest buyer of upstream oil-and-gas equipment. Texas producers literally need Mexican demand to keep associated-gas prices from cratering; U.S. liquefaction capacity covers only 9.5% of production. The old “U.S. deficit with Mexico” narrative?

It flipped into a surplus years ago. You can read more about this in my previous essay on energy. Opinion: Could Mexico make America great again?

The energy equation The Ember reports make the math deliciously clear. Hitting 45% clean electricity by 2030 would cut Mexico’s gas imports for power generation by 20% and save US $1.6 billion a year. Falling battery prices turn Mexico’s world-class sunshine into dispatchable power that can replace imported U.S. gas entirely in many places.

Cheaper, cleaner energy in Mexico makes every nearshored factory more competitive. It powers semiconductor plants (Foxconn/Nvidia’s giant Guadalajara server assembly), the auto industry and the exploding data-center boom (Microsoft’s $1.3 billion, AWS’s $5 billion, ODATA’s 400 MW campus). Mexico needs energy capital investment ASAP!

Energy is the multiplier for everything else in our series. Dr. Luis de la Calle brings the argument home. He constantly highlights how Asia knows this game cold: they do 65% of their intermediate-goods trade inside the region; we’re stuck at 48%.

If we want to compete with Asia, we must integrate vertically as a region. Energy is one of the three non-negotiable conditions (along with logistics and talent) for making that happen. Without competitive, abundant, regionally sourced power, the rules-of-origin incentives in USMCA stay half-baked — even counterproductive.

Asia’s dense energy-and-supply web keeps factories humming at low cost. We have the pipelines, the complementary resources, the rulebook and the geography — we just haven’t flipped the switch to “continental platform” yet. That brings us to the rulebook itself: USMCA, our legal backbone.

The agreement already treats energy trade as a complementary system, not a zero-sum fight. But Mexico’s latest energy reform has created real ambiguity in interpretation, and investors hate ambiguity more than they hate tariffs. We need to use the 2026 review to lock in clarity: make sure the recent Mexican reforms align with USMCA, fast-track cross-border electricity and renewable projects and create joint incen